JPMorgan Moved $4 Trillion on Blockchain. Nobody Noticed.

While crypto Twitter argued about NFT floor prices, JPMorgan quietly processed more than $4 trillion in payments through a blockchain network most of its own clients don’t think of as “blockchain” at all. That’s the story nobody in enterprise Web3 adoption is telling correctly in 2026, and it’s the one that actually matters if you run technology, treasury, or compliance at a large company.

Enterprise blockchain adoption in 2026 isn’t a comeback story. It’s a sorting story. A handful of single-institution platforms, Kinexys at JPMorgan and BUIDL at BlackRock among them, are processing real institutional money at real scale. Meanwhile, nearly every bank-consortium blockchain project built between 2018 and 2022 is either dead or has quietly ripped the blockchain out of its own architecture. Both things are true at once, and the difference between them tells you exactly where to place your next infrastructure bet.

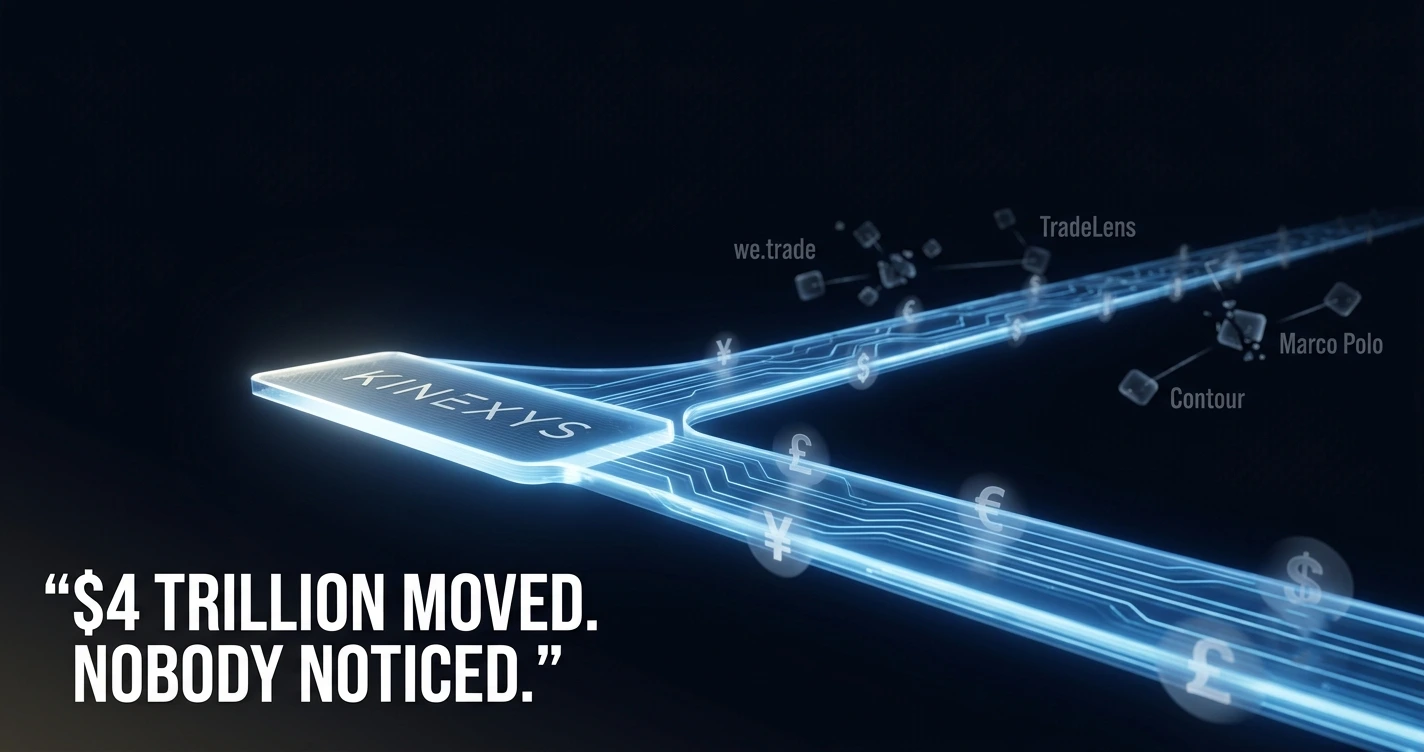

Kinexys: the $4 trillion ledger nobody calls Web3

Onyx became Kinexys in a rebrand back in November 2024, and the name change buried what should have been the bigger headline: JPMorgan’s blockchain payments network was already processing serious institutional volume, and it hasn’t slowed down since.

As of late June 2026, Kinexys added five Asia-Pacific currencies (Australian dollar, Hong Kong dollar, Japanese yen, Chinese renminbi, and Singapore dollar) to its Blockchain Deposit Account network, bringing the total to eight currencies alongside the dollar, euro, and pound. That’s not a pilot program expanding slowly. That’s a bank building out global rails.

The numbers back it up. JPMorgan says Kinexys has processed more than $4 trillion cumulatively since launch, with average daily volume now exceeding $7 billion. And the bank isn’t done. Zack Chestnut, Kinexys’s Global Head of Commercial, has pointed to a strong pipeline of institutional clients as the bank works toward doubling daily throughput past $10 billion.

Here’s the catch nobody advertises: Kinexys isn’t decentralized in any sense the original Web3 pitch promised. It’s JPMorgan’s permissioned ledger. Clients don’t hold their own keys. There’s no exit right, no token governance, no trust-minimization between competing parties. It’s a bank-owned database that happens to run on blockchain rails, and that distinction turns out to be the whole story.

BlackRock’s BUIDL and the tokenized treasury boom

If Kinexys proves banks can run blockchain infrastructure at scale, BlackRock’s USD Institutional Digital Liquidity Fund (ticker BUIDL) proves asset managers can too. Launched in March 2024, BUIDL became the fastest tokenized fund to reach $1 billion in assets, hitting that mark within seven months.

By Q2 2026, tracker estimates put BUIDL’s assets under management somewhere between $2.3 billion and $2.5 billion, depending on whether you’re pulling from rwa.xyz, Token Terminal, or secondary crypto-media snapshots. The range matters more than any single number here. This category moves fast enough that any figure is stale within weeks.

BUIDL now runs across eight or nine blockchain networks depending on the source, including Ethereum, Solana, Polygon, and Avalanche. It’s not alone. Franklin Templeton, Ondo’s OUSG, Circle’s Hashnote USYC, Apollo, Hamilton Lane, and even JPMorgan’s own MONY and JLTXX money market products are all live tokenized treasury vehicles competing for the same institutional cash.

| Category | Estimated size (mid-2026) | Source basis |

|---|---|---|

| BlackRock BUIDL AUM | ~$2.3B to $2.5B | rwa.xyz / Token Terminal |

| Tokenized Treasury/MMF segment | ~$10B to $15B | rwa.xyz-derived trackers |

| Total on-chain RWA market | ~$22B to $32B | rwa.xyz-derived, multiple outlets |

Every one of those ranges gets rounded up in vendor blog posts into breathless “$16 trillion by 2030” projections, often attributed loosely to consulting firms. Treat those as long-range forecasts, not current facts. The real number today is closer to the tens of billions, concentrated almost entirely among the largest asset managers on earth.

The trade-finance graveyard: why consortiums keep dying

Here’s where the “quiet enterprise win” narrative needs a hard correction, because the industry’s most ambitious multi-bank blockchain experiment didn’t quietly win. It quietly collapsed, four separate times, in less than two years.

- We.trade, an 11-bank European consortium backed by IBM, HSBC, Deutsche Bank, Santander, and UBS, shut down in June 2022 citing insufficient network growth.

- TradeLens, the Maersk and IBM shipping platform launched in 2018, was discontinued in November 2022 after failing to reach commercial viability.

- Marco Polo Network, built on R3 Corda with more than 30 banks including Commerzbank, BNY Mellon, and SMBC, entered insolvency in Ireland in February 2023 with total debts of €5.2 million, after a roughly $12 million Bank of America investment fell through.

- Contour, a letter-of-credit digitization platform backed by nine banks including HSBC, BNP Paribas, and Standard Chartered, shut down in November 2023, reportedly processing only 60 to 70 transactions a month before closure.

Only one of the five major consortium platforms, Komgo, is still standing, and it survived by dropping blockchain entirely in favor of a centralized database. Four dead, one that abandoned the technology it was built on. That’s not a rounding error. That’s a structural failure of the entire model.

“They couldn’t scale.” Joshua Kroeker, former head of product development for trade finance at HSBC, speaking to Digital Finance Group about Contour

Kroeker’s read on why is worth sitting with: these networks were built solving a narrow problem that only worked if every competitor joined the same platform, and competitors almost never do that voluntarily. He’s not blaming the technology. He’s blaming the governance model that required rivals to trust each other with shared infrastructure.

IBM Food Trust’s second life, courtesy of the FDA

The Walmart mango story gets quoted constantly and almost never correctly. Yes, IBM and Walmart famously cut mango traceability from seven days down to 2.2 seconds using Hyperledger Fabric, back around 2018. What gets left out is that Walmart reportedly paused its blockchain food-tracking mandate around December 2022, part of the same wave of retrenchment that killed TradeLens. So is IBM Food Trust dead? No, and the reason it survived is instructive. It’s still a commercially sold product in 2026, now rebranded under the IBM Supply Chain Intelligence Suite and marketed specifically around compliance with the FDA’s Food Safety Modernization Act Rule 204(d), which required covered food entities to have enhanced traceability recordkeeping in place by January 20, 2026.

That’s the tell. Food Trust didn’t survive because companies fell back in love with blockchain idealism. It survived because a federal deadline forced compliance teams to buy traceability tooling, and distributed-ledger backends happened to be underneath it. Regulation, not conviction, kept the lights on.

The real pattern: ownership beats decentralization

Step back and the pattern across every example here is identical. Single-owner infrastructure survives. Multi-party consortium infrastructure dies. That’s almost the exact opposite of what Web3’s original pitch promised enterprises back in 2018.

“Blockchain just really hasn’t hit the heights that were promised.” Adrian Leow, VP Analyst, Gartner, to CIO.com, March 2025

Leow’s comment came alongside a broader signal worth flagging: Gartner published its most recent dedicated Blockchain and Web3 Hype Cycle in 2024, and as of 2025 the firm has indicated it may not publish another standalone one, because analyst-level interest has faded. That’s notable timing, because it means Gartner effectively stopped watching right as Kinexys and BUIDL’s real production numbers started climbing.

Other voices from the same CIO.com reporting reinforce the skepticism. Trevor Fry, an IT consultant and fractional CTO, argued that blockchain “doesn’t solve a problem that many companies or people have” in most business contexts. Salome Mikadze, co-founder of Movadex, put it more bluntly: outside a few supply-chain and data-sharing niches, blockchain “is on the shelf for now” for most enterprises.

Both critiques are fair, and both miss the narrower point. Nobody serious is claiming blockchain solved a universal enterprise problem. What survived is a specific pattern: single-institution settlement and tokenization infrastructure that a client can simply plug into, with no governance negotiation required. That’s a much smaller claim than the original Web3 pitch, and it happens to be the one backed by trillions of dollars in real volume.

- CFOs and treasury leads: Ask your existing banking partners whether they offer blockchain-deposit-account or programmable-payment products before funding anything custom.

- CTOs: Don’t fund a multi-party consortium expecting network effects. Every one of them has failed or abandoned blockchain. Single-vendor infrastructure is the model that works.

- Compliance leads in regulated supply chains: The FSMA 204(d) deadline already passed in January 2026. If your traceability tooling isn’t sorted, that’s a live compliance gap, not a future one.

One more honesty check worth building into your planning: even the winners here are concentrated at the very top of the market. There’s limited public evidence yet of mid-market or non-financial enterprises replicating what JPMorgan and BlackRock have done independently. Most of the momentum right now is JPMorgan-scale and BlackRock-scale, not broadly distributed across the Global 2000. A frequently cited figure, attributed secondhand to Gartner via industry blogs rather than Gartner’s own published research, claims 25% of Global 2000 companies will run blockchain in production by the end of 2026, up from 11% in 2024. Treat that one as directionally interesting but not independently verified.

FAQ: enterprise Web3 in 2026

Is Web3 dead in the enterprise?

Not the infrastructure side. Consumer-facing Web3 (NFTs, DAOs, token speculation) has largely stalled, but narrow use cases like bank-led settlement (JPMorgan’s Kinexys, over $4 trillion processed) and tokenized treasury products (BlackRock’s BUIDL) are in active, growing production use as of 2026.

What happened to IBM Food Trust and Walmart’s blockchain program?

Walmart paused its blockchain food-tracking mandate around December 2022 during a broader enterprise retrenchment. IBM Food Trust remains commercially active in 2026, now marketed around FDA FSMA Rule 204(d) traceability compliance, which took effect January 20, 2026.

Why did enterprise blockchain trade-finance platforms fail?

Four of five major bank-consortium platforms, we.trade, TradeLens, Marco Polo, and Contour, shut down between 2022 and 2023. The common cause was weak network effects and the difficulty of getting competing banks to share one shared platform, not a failure of the underlying technology itself.

What is JPMorgan Kinexys used for?

Kinexys, formerly known as Onyx, is JPMorgan’s permissioned blockchain platform for 24/7 cross-border payments, programmable treasury operations, and asset tokenization. Institutional clients include Siemens, BMW, and Mitsubishi Corporation, and it has processed more than $4 trillion since launch.

How big is the tokenized real-world asset market in 2026?

Estimates vary by tracker, but the total on-chain RWA market, spanning Treasuries, private credit, and real estate, sat roughly between $22 billion and $32 billion as of mid-2026, according to rwa.xyz-derived data cited across multiple industry sources.

Where this goes next

The story enterprise Web3 needed to tell in 2026 isn’t a redemption arc. It’s a sorting exercise, and the sorting is basically done. Single-owner platforms that clients plug into without governance friction are scaling into the trillions. Multi-party consortiums that needed competitors to cooperate are, with one exception, gone.

Watch three things over the next 6 to 18 months: whether Kinexys actually crosses that $10 billion daily volume target, whether a mid-market or non-financial enterprise manages to replicate the single-owner model outside banking and asset management, and whether the FSMA 204(d) enforcement period pushes other regulated industries toward the same “mandate, not idealism” adoption path that rescued IBM Food Trust.

None of this is the decentralized future Web3 originally promised. It’s something narrower, more boring, and, it turns out, considerably more durable.

Want more analysis like this in your inbox? Subscribe to The Neural Loop for weekly breakdowns of where enterprise technology is actually heading, not just where the headlines say it’s going.

Related reading: MakerDAO Sky Governance 2026: the $400M No-CEO Vote · Browse more in Blockchain

Sources: JPMorgan Newsroom, CoinDesk, S&P Global Market Intelligence, Ledger Insights, Global Trade Review, CIO.com, PYMNTS. Figures involving tokenized asset market size are ranges attributed to named trackers (rwa.xyz, Token Terminal) and should be treated as estimates, not fixed totals.